Monthly Archives: August 2022

Arizona Real Estate update 8.8.2022

Reply

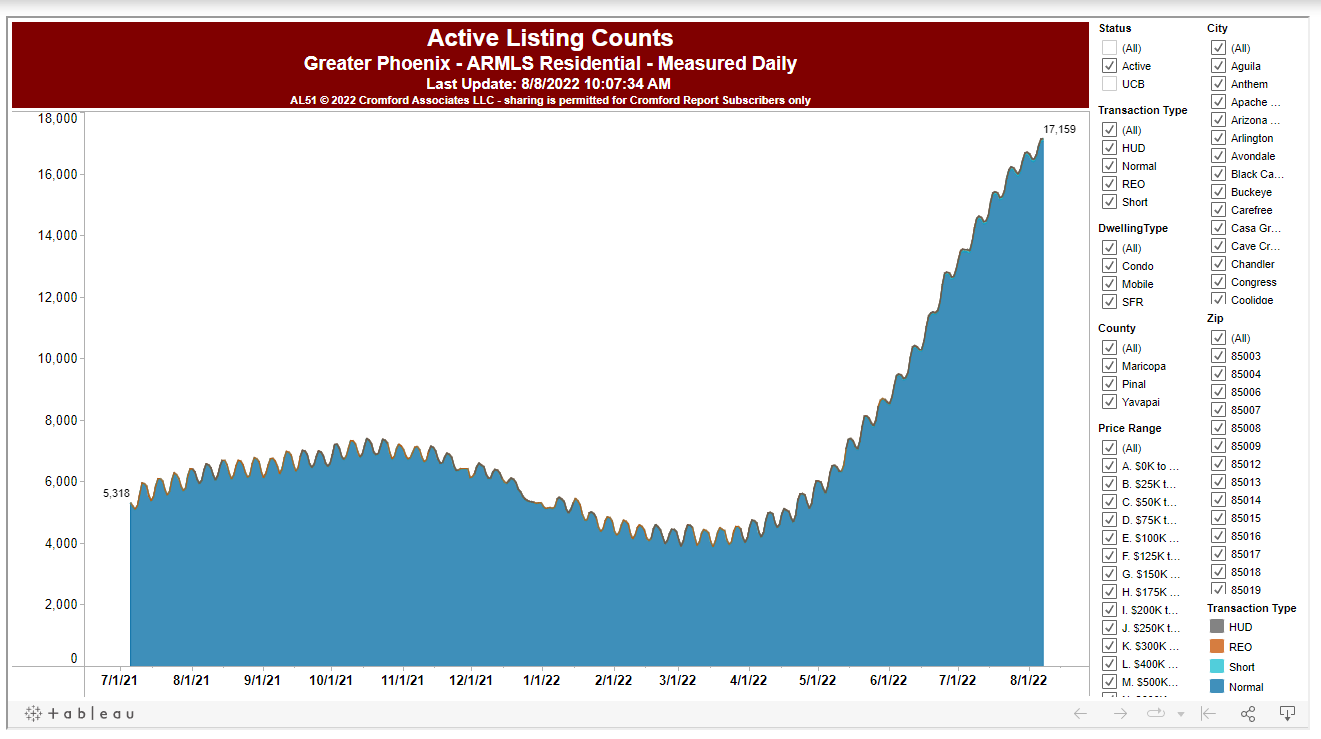

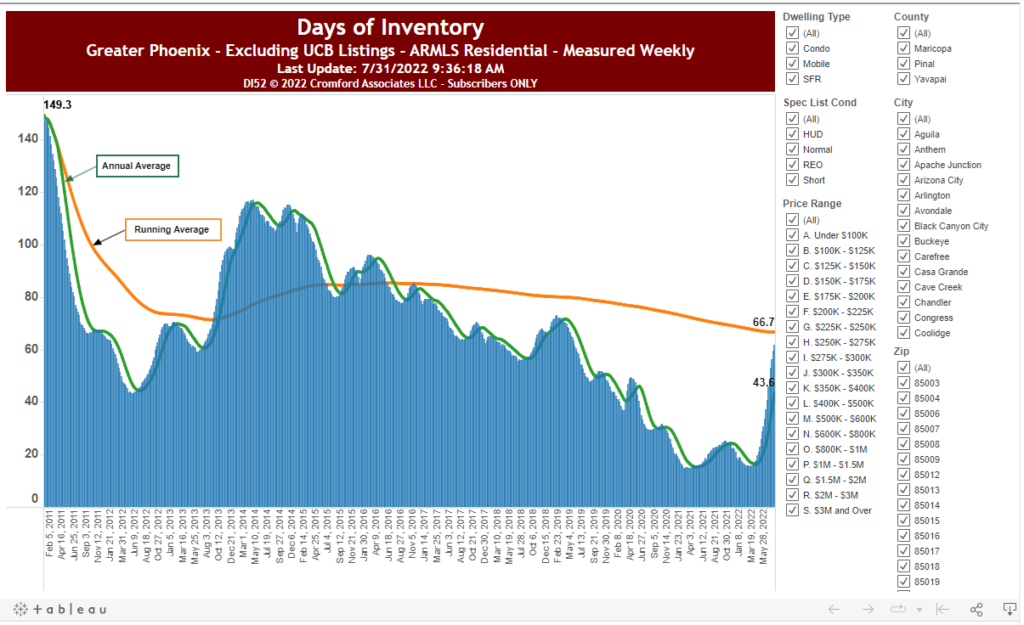

Six months ago some had the opinion, ‘this time is different. Their primary argument was that supply didn’t exist so housing prices could not fall that significantly. I always pushed back, you don’t know how many people are holding second or third houses as rentals. Or how many people bought Airbnb properties because ‘houses always go up in value? Well, now we are finally seeing people unload those houses. Where they came from for sure, who knows. But they are coming out of the woodwork. The good news is we are not yet back to the levels of inventory that we saw back ding the 2008 collapse. The peak houses for sale back then were somewhere just shy of 60k. All of the old data can be found on ARMLS. It would be nice if someone compiled it into graphs.

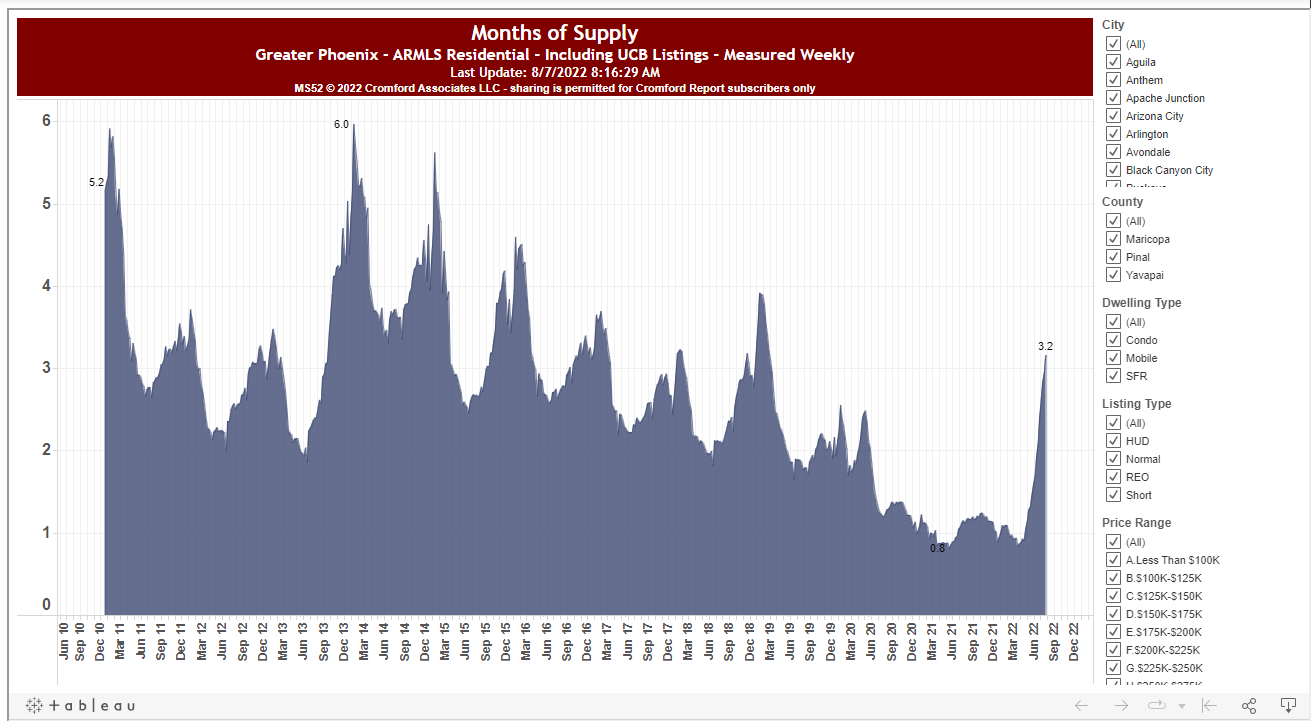

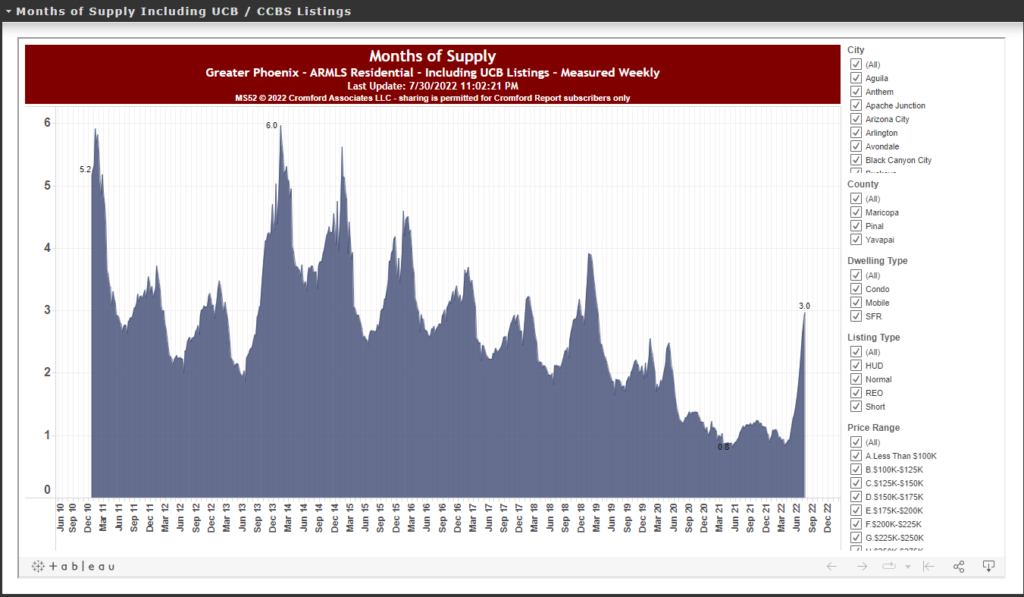

The months of supply now sit at 3.2. As I’ve indicated before supply is cyclical and we should see this peak around Jan-Feb, all else being equal.

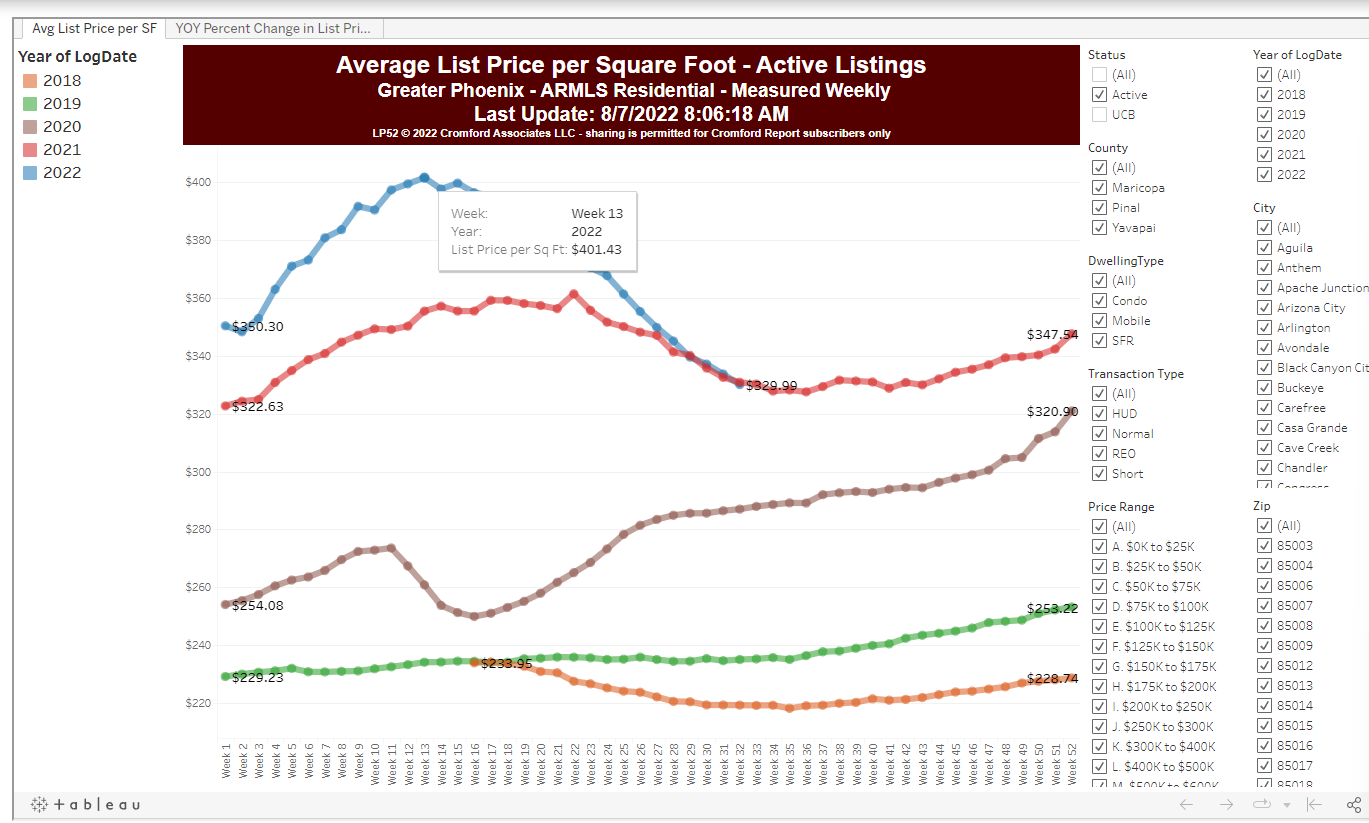

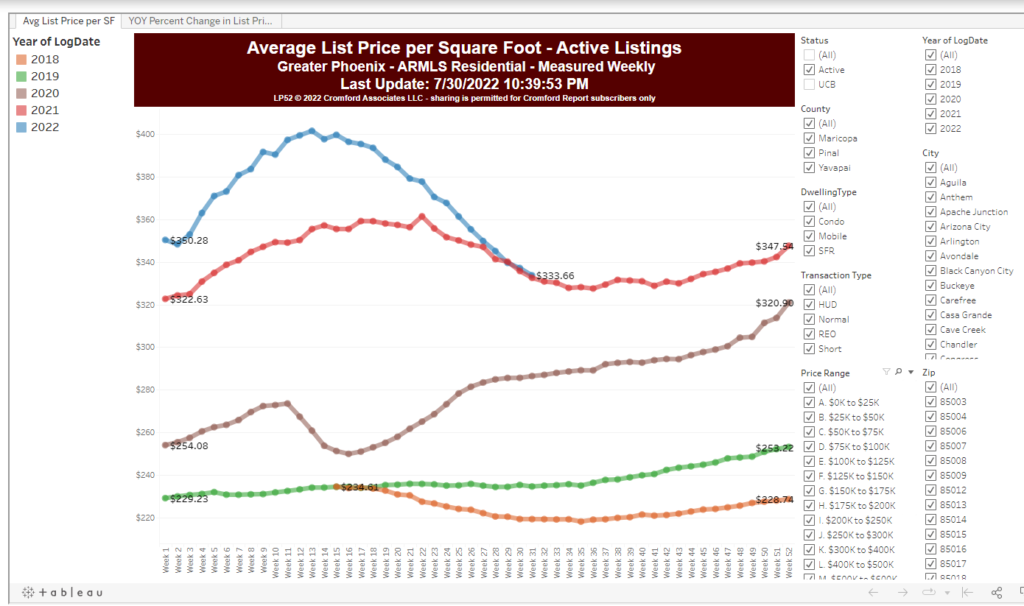

House prices peaked at $401.43/sq ft in March. Since then they have declined about 18% to $329/ sq ft.

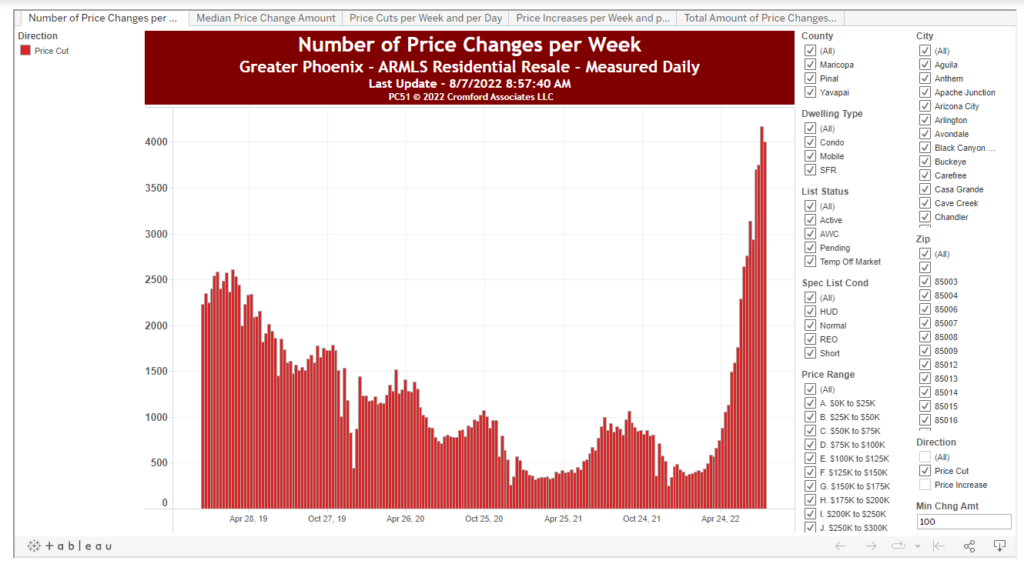

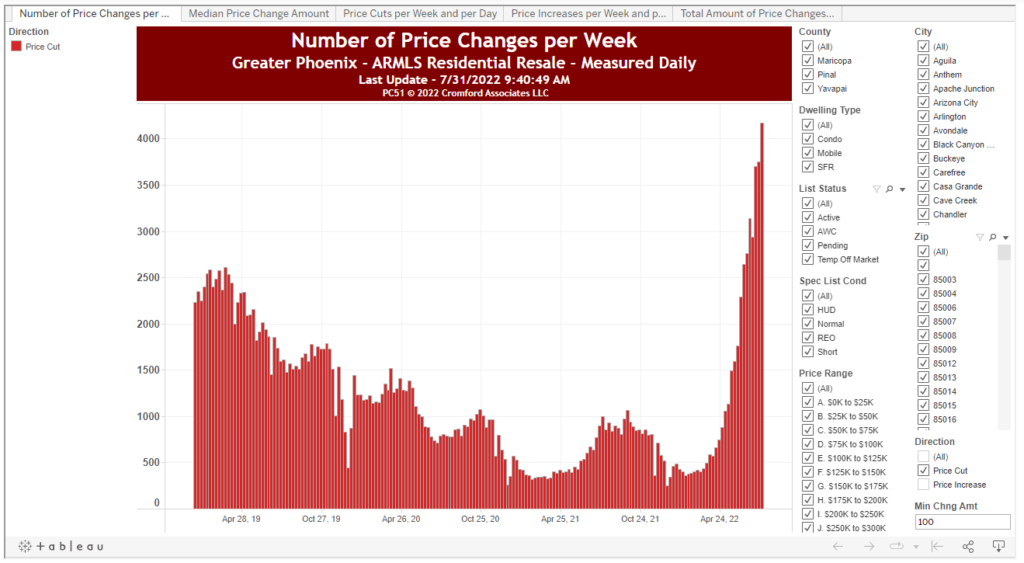

One of the key things I’m keeping an eye on is the number of price cuts per week.

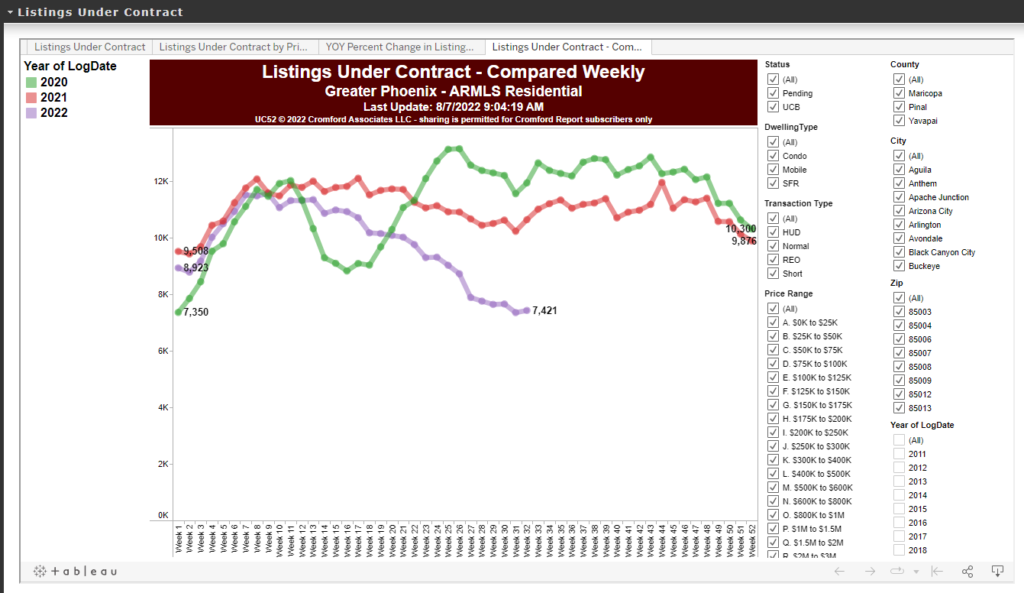

It is still elevated at 4,006. This represents 25% of the listings for sale. One in every four people who are selling houses has had to cut their price in the last week. The psychological implications of this I think are huge. People are not going to buy if they think prices will continue to decline. Listings under contract continue to decline and currently sit at 7,421.

To put this in perspective in Q4 of 2007 the lowest this level dropped to was 8,898. You could however argue that this low number is due to low inventory.

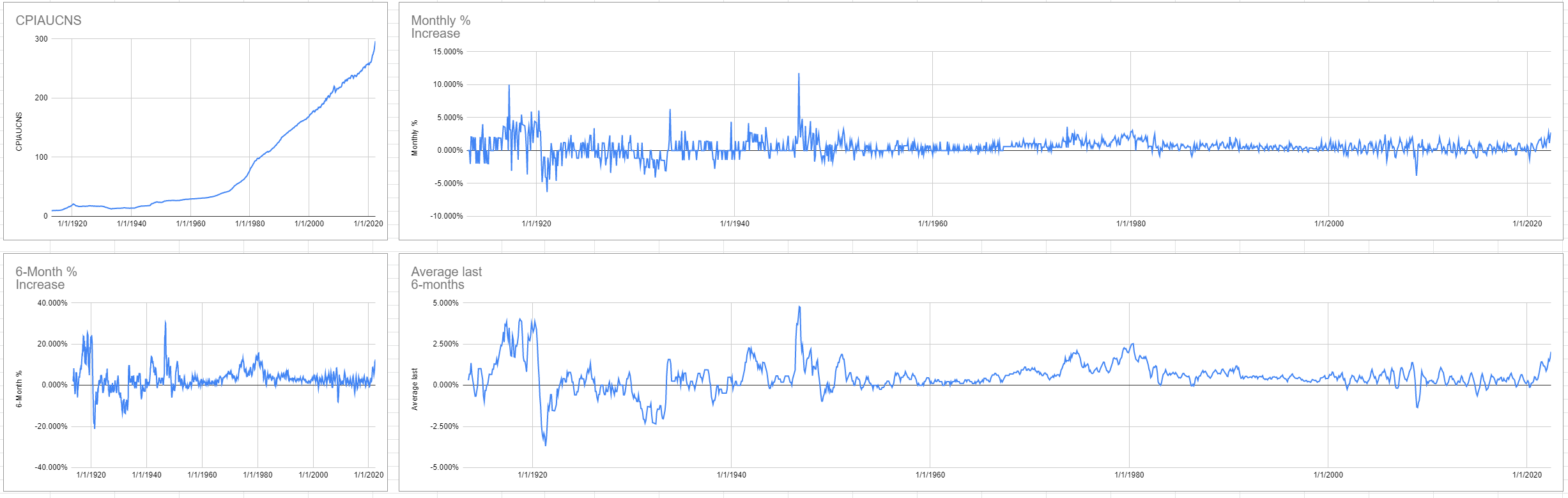

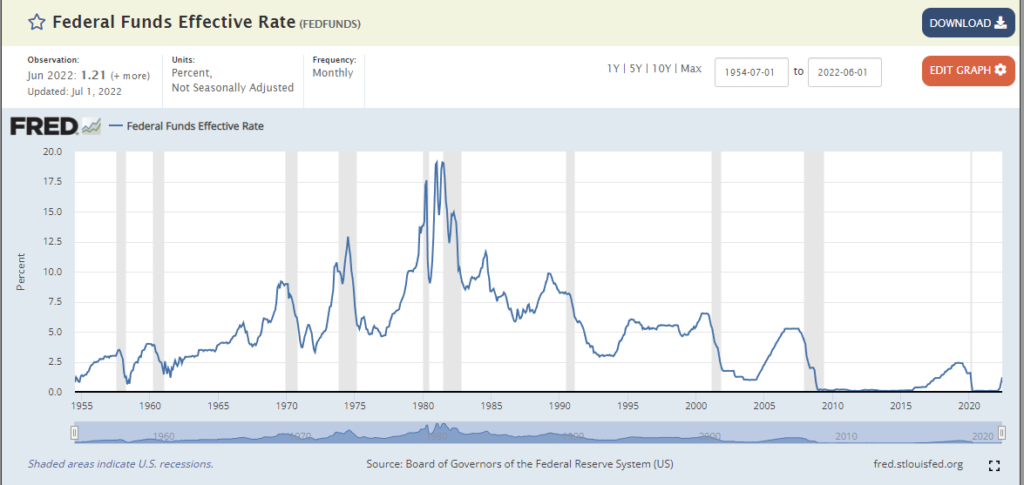

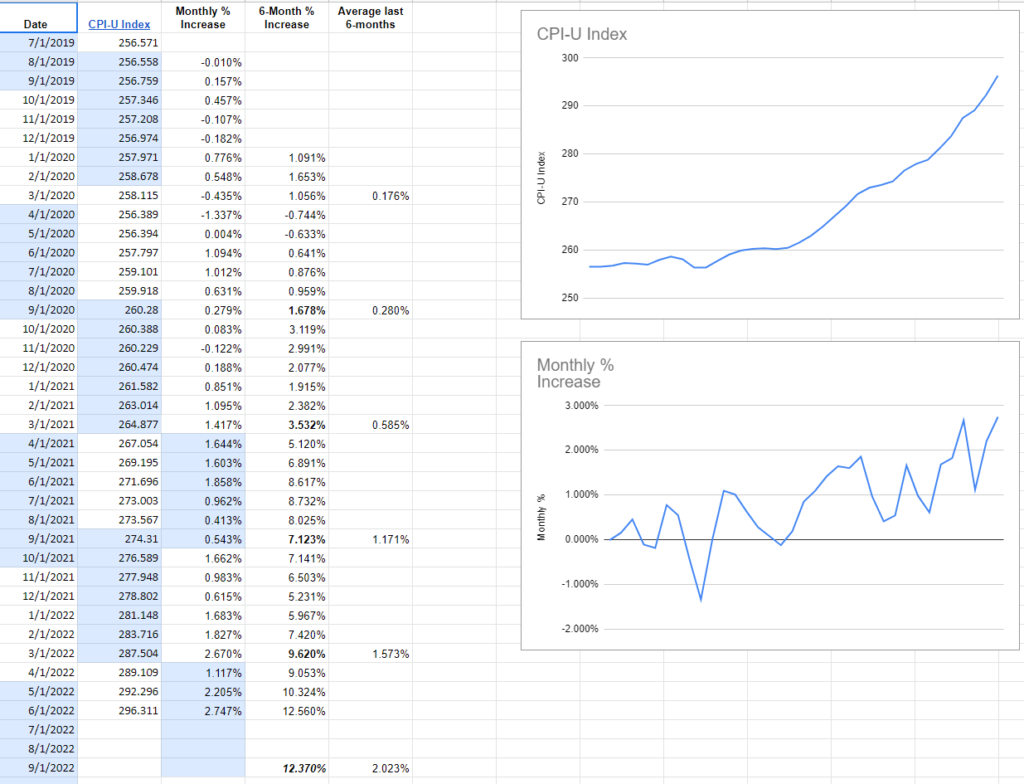

I follow CPI(inflation) pretty closely for a different investment that I’m working on.

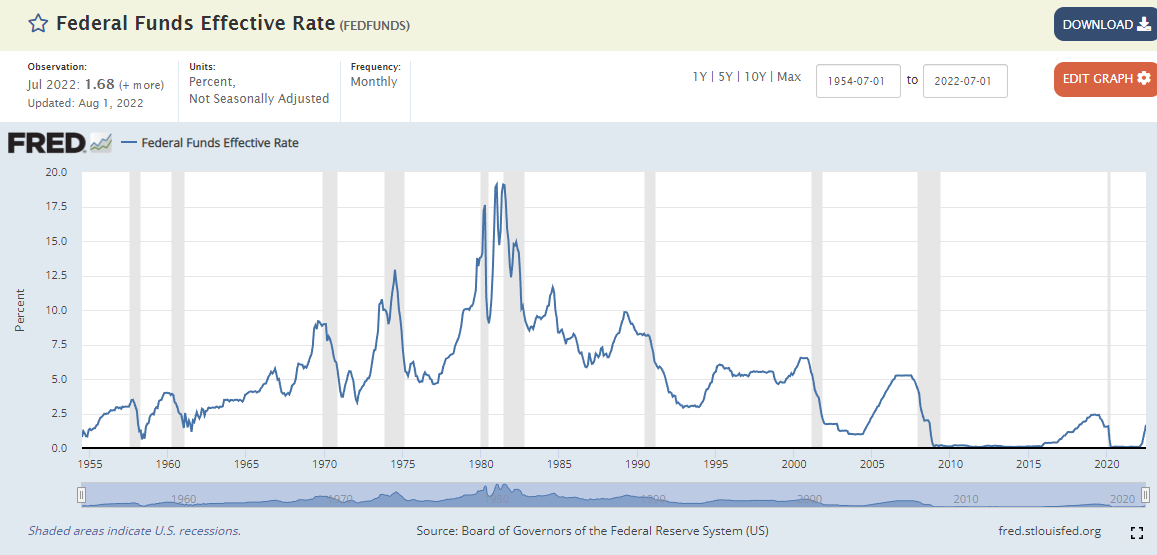

The FED is afraid of inflation. In fact, I think it’s the only thing keeping them in check. It is the main driver behind them raising rates and why they will continue to do so. I’m eagerly waiting for the July CPI report which will be released on August 10th. If CPI is continuing up the FED will respond accordingly. Until the FED stops raising rates I would be very cautious about investing in any asset class.

Arizona Real Estate update 8.1.22

People are still slashing their listing prices. It increased to its highest level this week, 4,172. This will continue to put huge downward pressure on prices.

We have exactly 3 months of supply also going to put downward pressure on prices. The number I’m waiting for this to break is 3.9. Once this happens will have the most supply since 2016. I expect this will continue upward until Jan-Feb of ’23 (it’s cyclical).

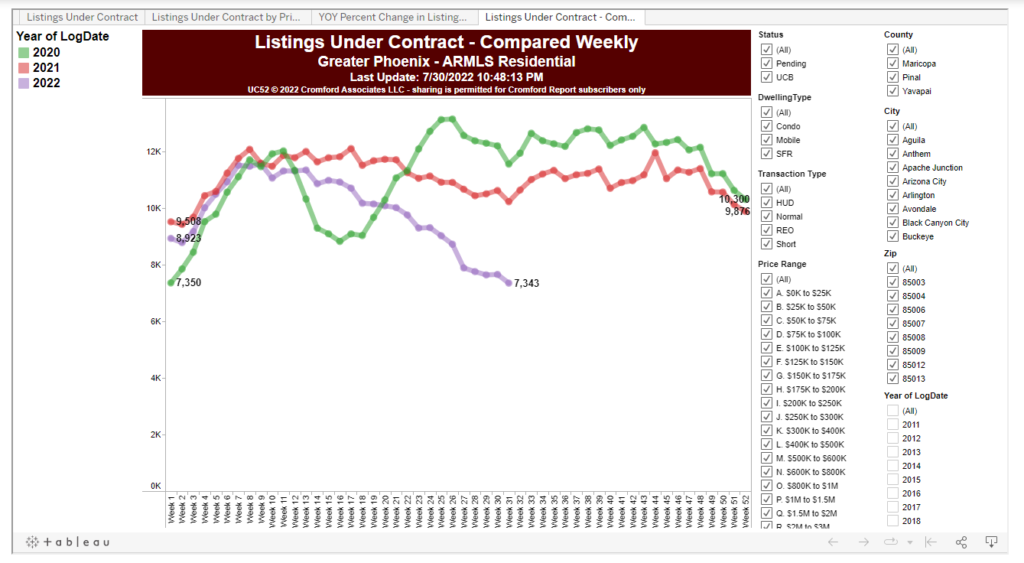

The number we should be watching now is listings under contract. It sits this week at 7,343. This is the lowest it’s been for at least 3 years. I don’t have data that goes back any further. This number will tell you where the ‘bottom’ is because it means people started buying again. Right now they still appear to be sitting on the sidelines.

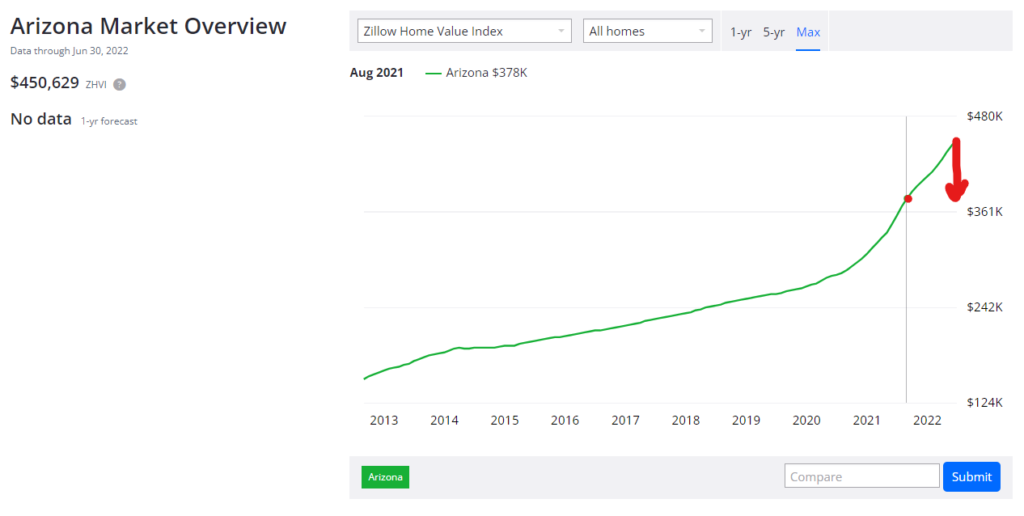

Listing prices are where they were a year ago. I’m not sure who is running things over at Zillow but their estimates don’t show any downturn. This appears to me to be highly inaccurate. I would not trust your ‘Zestimate’ right now. It seems their algorithm has no method to adjust for a ‘listing price’ variable.

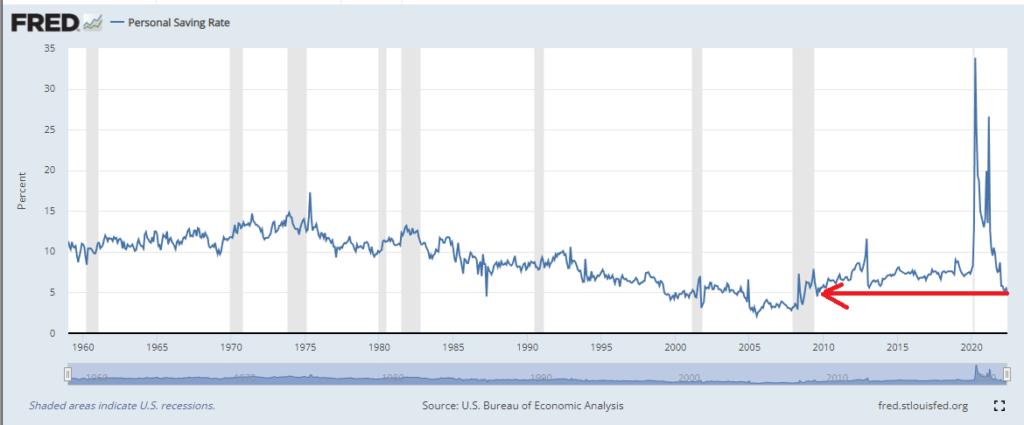

It’s understandable why houses are not moving. Since the huge injection of capital into the system in early 2020(Covid) people are broke again. This can be seen in the personal savings rate. It is the lowest since 2009. I think this will also have an adverse effect on retail stocks. I’m willing to bet this will continue to decline to all-time lows in the next year or two. America is addicted to stimulus. With Fed rates going up the balance sheet of individuals is going to deteriorate.

The question now is will the Fed continue to raise rates or pause as Powell hinted at last week?

I’m a huge believer in I Bonds right now. They are one of the most solid investments you can make. They yield 9.62% risk-free. That being said I follow the inflation numbers pretty closely so I can determine what their new rate will be, come November 1st. There is nothing that indicates a slowdown in CPI-U(inflation). The next report is due on August 10th. I imagine that one won’t be friendly and the Fed will be back on track to raise rates for their September meeting. If inflation continues on its current trajectory then I bonds will yield north of 12% in November.

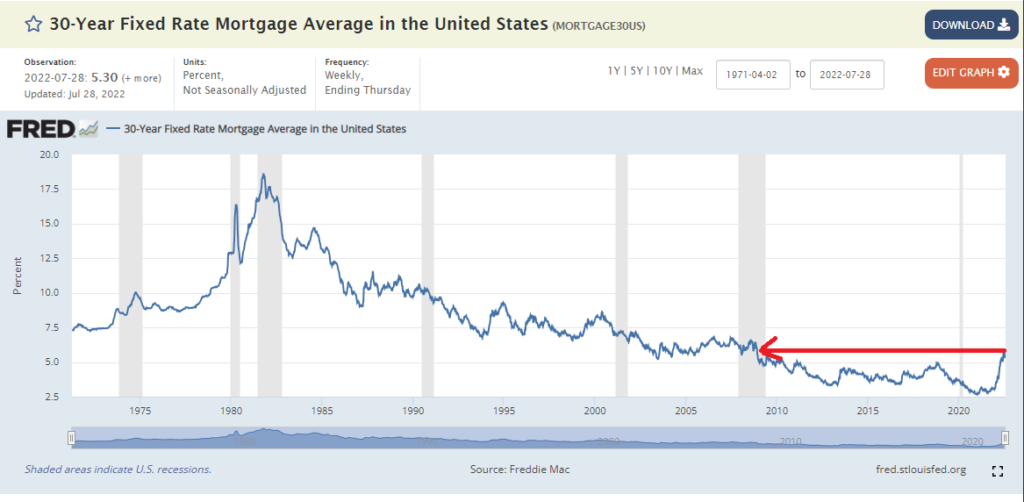

Mortgage rates are also where they were back in 2008/2009. With housing values up and rates up people cannot afford this market.